The fund still sits on $89k cash in bank, or 70% of the funds assets. The trustees recognise that the funds performance may have been better over the last year if their exposure to shares had of been greater; however they note the following:

- Earnings growth has outpaced market growth over the last three years; based on market price verus future earnings the market is now "cheaper" than three years ago.

- The trustees have been evaluating share purchases and simply have been unable to find any shares that they were comfortable buying for the long term, or in a couple instances the shares prices moved to quickly.

- The trustees are currently looking at some shares; including NAB, FLT and MMC.

- We have been looking for better vehicles for the funds cash holdings, but none of the current cash alternatives offer attractive risk to reward at the moment.

- The fund has a very long term view and one year of under performance will not force the trustees in to the market.

Sunday, April 09, 2006

Saturday, March 04, 2006

Diversify - why?

Almost everyone says to diversify. I have not put enough thought or study of diversification to know whether it is best for me or not. However, until I do, the easiest path is to follow the wisdom of the masses and diversify.

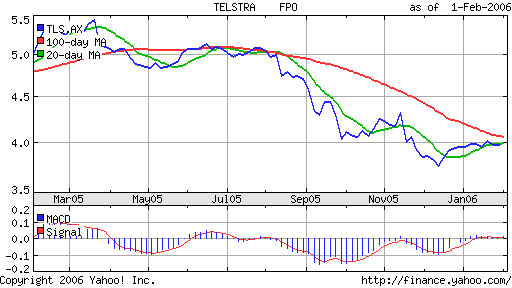

As a trustee I note the Super Fund is as woefully diversified as can be. One listed company and cash accounts. With 33% of the fund invested it Telstra I feel it necessary to explain this position.

One of the reasons for taking control of our Super was to control diversification across all our long term assets. Under a total assets comparison Telstra makes up under 5% of assets, which is comfortably under our limit of 10%.

Telstra has a complex risk reward scenario, but we hold it to be a good long term buy and dividend paying share for many years to come.

With total fund diversification and assets utilisation in mind the super fund will sell 1 NAB put if NAB is over $36 at options expiration 30 March 2006. Aim will be good price on $36 Put, with $37 Put considered if excellent price over .70 can be gained. As always with Naked Puts the aim is to sell at a price we are happy to buy at, ie getting paid for a limit order.

As a trustee I note the Super Fund is as woefully diversified as can be. One listed company and cash accounts. With 33% of the fund invested it Telstra I feel it necessary to explain this position.

One of the reasons for taking control of our Super was to control diversification across all our long term assets. Under a total assets comparison Telstra makes up under 5% of assets, which is comfortably under our limit of 10%.

Telstra has a complex risk reward scenario, but we hold it to be a good long term buy and dividend paying share for many years to come.

With total fund diversification and assets utilisation in mind the super fund will sell 1 NAB put if NAB is over $36 at options expiration 30 March 2006. Aim will be good price on $36 Put, with $37 Put considered if excellent price over .70 can be gained. As always with Naked Puts the aim is to sell at a price we are happy to buy at, ie getting paid for a limit order.

Wednesday, February 22, 2006

Continue to hold Telstra and buy Argo

We calculate the overall dividend plus franking credits return to our SMSF is 12.1%. This is an excellent return and we are happy to remain long Telstra. The major risk to this investment is a reduced dividend pay out.

Trustees will further investigate Argo Investments with view to buy a stake to allow participation in share purchase scheme.

Trustees will further investigate Argo Investments with view to buy a stake to allow participation in share purchase scheme.

Saturday, February 18, 2006

Investment in Argo Investment

The fund will make an inital small investment in Argo Investments shares. The initial investment will be to facilitate participation in their Share Repurchase plan and other attractive benefits as listed below.

Low Management Costs

No management fees are charged by Argo and being a listed company, only normal stockbroker charges apply when shares are purchased and sold. For the year ended 30 June, 2005 total operating costs were 0.15% of total assets at market value.

Franked Dividends

Argo pays dividends in March and September each year. Imputation credits on dividends received by Argo are passed on through the fully franked dividends paid to Argo shareholders, with all shareholders benefiting from the associated tax credits. Certain Australian share holders can also claim a tax benefit where the dividend is sourced from a LIC capital gain.

Share Purchase Plan

Argo has a Share Purchase Plan which enables shareholders to invest up to $5,000 a year in additional shares, currently at a 2.5% discount off the market price. Participation in the SPP is entirely at the option of the shareholders and no transactional costs apply.

Dividend Reinvestment Plan

Argo has a Dividend Reinvestment Plan, which is currently offered to eligible shareholders at a 2.5% discount off the market price. Participation in the DRP is again entirely optional and no transactional costs will apply.

Share Issues

Argo also has a history of making attractively priced new issues of shares to our existing shareholders.

Combined with their outperformance of All Ords Accumulation INdex for 5,10,15 and 20 years.

Initial investment of between $2-$5k will be made and then a regular investment of $400-$800 per month to dollar cost average in to the stock.

Wednesday, February 08, 2006

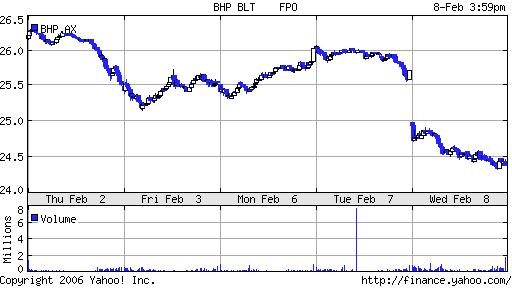

BHP position not taken

Due to circumstances we did not sell the BHP puts as planned on Monday 23rd Jan. The stock price then took off from a low of 24.23 on Monday to peak at 26.63 a week later and hovered in the low 26 range until today, when gravity and sanity returned with the stock dropping over 5%. After reading comments by the Intelligent Investor we will now closely watch both BHP and Rio Tinto for an entry or attractive Put position.

Thursday, February 02, 2006

Holding Telstra

The Trust will continue to hold Telstra. The latest pop in share price on news of T3 in encouraging that the trustees original investment thesis will be fulfilled. The trust will be able to sell some of it's holding over the average paid and will have netted the attractive dividends for that period. Despite being in the troubled Telecommunications industry the trustees had believed if as the largest shareholder the government had known any information that would have led them to believe $5.25 for not a realistic price for T3 then they would have stated that and lowered their price accordingly. However, despite having the knowledge they did not lower their price target. This resulted in the Trusts purchase of a volume and portfolio percentage of the shares far greater than they would normally allocate to an individual share. The other contributing factor was the announcement of the special dividend combining to form $.40 a year in franked dividend. Was that a bribe to unload shares by the company?

At any rate the dividend has been better than interest and as stated the trustees believe they will get to sell above the average price, some time in the future. They will look at call options on Telstra.

At any rate the dividend has been better than interest and as stated the trustees believe they will get to sell above the average price, some time in the future. They will look at call options on Telstra.

Saturday, January 21, 2006

Buy BHP - are we mad

BHP is the worlds largest resource company, by a long shot. It is bigger than number 2 and 3 combined. It's price has doubled in a couple of years. The world is in a mad commodities boom and analysts are projecting earning based on historical metal prices.

The trustees believe that the fund requires exposure to the commodities boom. We realise that it may be a rocky road, but in the long term China and India need the commodities to fuel their growth so there is little downside risk in BHP.

Therefore, the fund will Sell to Open BHPWZ Feb 24 Puts which had a last trade price of .48. If the price of BHP falls and the puts are exercised the costs price will be 23.52 (excluding commissions), compared to a closing price of 24.45. At this time and with the recent peak in the price the fund will only sell 1 option.

Return on risk is about 2% for 31 days holding.

We have been looking at ways to get exposure to the commodities boom as the super members do not have any other exposure to commodities at this point. The tipping point was the Feb 2006 issue of True Wealth by Steve Sjuggerud, strongly recommending BHP.

Dividends are a paltry 1.6% or so, 100% franked. Last ex dates were 28 Feb 05 and 5 Sep 05.

Need to check recent filing for next ex date. Neither ASX or income investor list any announced date.

The trustees believe that the fund requires exposure to the commodities boom. We realise that it may be a rocky road, but in the long term China and India need the commodities to fuel their growth so there is little downside risk in BHP.

Therefore, the fund will Sell to Open BHPWZ Feb 24 Puts which had a last trade price of .48. If the price of BHP falls and the puts are exercised the costs price will be 23.52 (excluding commissions), compared to a closing price of 24.45. At this time and with the recent peak in the price the fund will only sell 1 option.

Return on risk is about 2% for 31 days holding.

We have been looking at ways to get exposure to the commodities boom as the super members do not have any other exposure to commodities at this point. The tipping point was the Feb 2006 issue of True Wealth by Steve Sjuggerud, strongly recommending BHP.

Dividends are a paltry 1.6% or so, 100% franked. Last ex dates were 28 Feb 05 and 5 Sep 05.

Need to check recent filing for next ex date. Neither ASX or income investor list any announced date.

Subscribe to:

Posts (Atom)